The global oil market in 2025 stands at a critical juncture, marked by an emerging supply surplus against demand. Key factors shaping the market include evolving US-Russia relations following Trump's election victory, contrasting demand patterns between India and China and OPEC+'s strategic responses to price pressures. With Brent crude expected to trade within a $75-85 per barrel range, higher in the first half before facing downward pressure, these dynamics suggest a year of significant market realignment ahead.

A Pivotal Moment in Geopolitical Dynamics

As 2025 begins, the global oil market stands at a geopolitical crossroads. The Biden administration's exit is marked by unprecedented sanctions on Russian energy, targeting key producers and trade networks. However, Russia's adept evasion tactics, including alternative trade mechanisms, might mitigate the impact, with major buyers like China and India potentially continuing purchases in non-dollar settlements.

The US election outcome, with Trump's return, adds another layer of complexity. His commitment to ending the Russia-Ukraine conflict could reshape geopolitical dynamics, potentially reducing the risk premium in oil prices. Yet, the transition period might see increased market volatility as both sides manoeuvre for advantageous ceasefire terms.

Looking further ahead, de-escalation in the conflict could lower geopolitical risks, reshaping oil trade patterns. However, persistent tensions in the Middle East, coupled with Trump's possible hardline stance on Iran, suggest that geopolitical factors will continue to significantly influence oil prices in 2025.

Supply Side: From Tight Balance to Oversupply

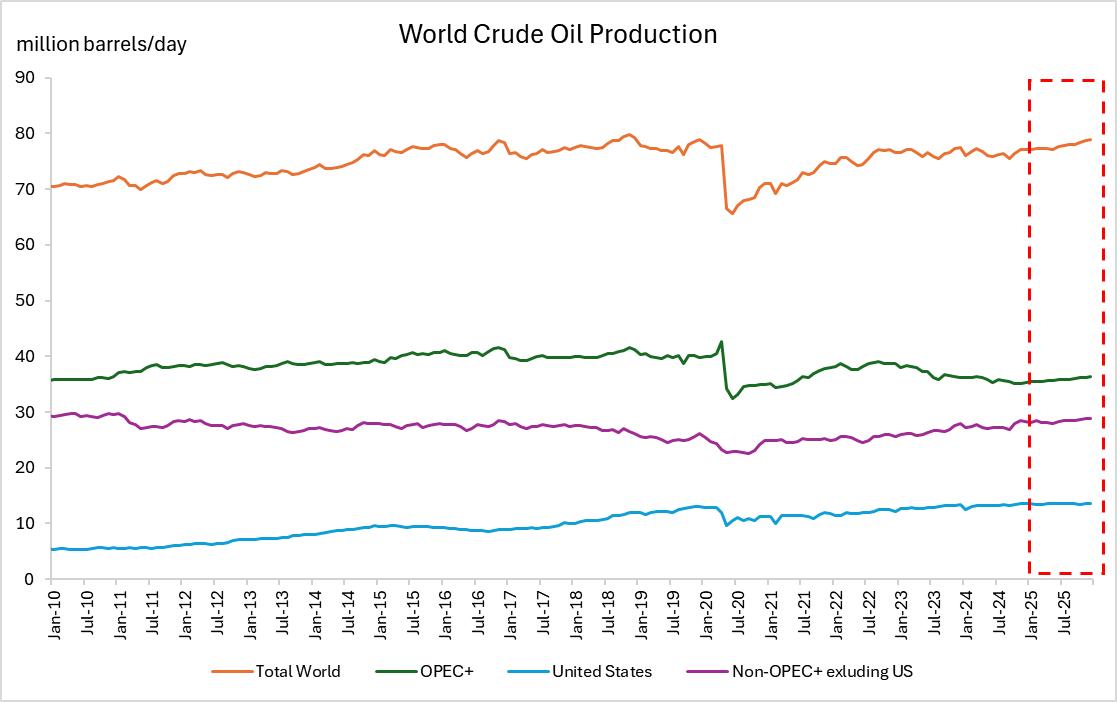

Looking ahead to 2025, global oil supply is expected to increase by 1.7 million barrels per day, primarily from non-OPEC producers from EIA estimates. However, the US growth momentum is predicted to slow, building on the record-high production levels of 2024. This moderation is due to several factors:

· Delayed Effect: After reaching high production levels in 2024, maintaining growth requires drilling more new wells due to the depletion of existing ones. The reduction in new drilling rigs in late 2024 will gradually impact production in 2025.

· Technological Advances: The space for efficiency improvements narrows and the availability of prime drilling sites decreases, making it harder to increase per-well output.

Considering these elements, US oil production is expected to remain relatively stable at high levels in 2025, unless oil prices significantly rise, prompting increased capital investment.

Non-OPEC countries are projected to contribute an additional 610,000 barrels per day of production growth, with Brazil's deep-water projects, Guyana's Stabroek Block development and increased Canadian oil sands output following the TMX pipeline startup being key sources. Norway's North Sea projects, Argentina's shale oil and Mexico's shallow water projects will also add to the supply.

Source: EIA, Tradingkey.com

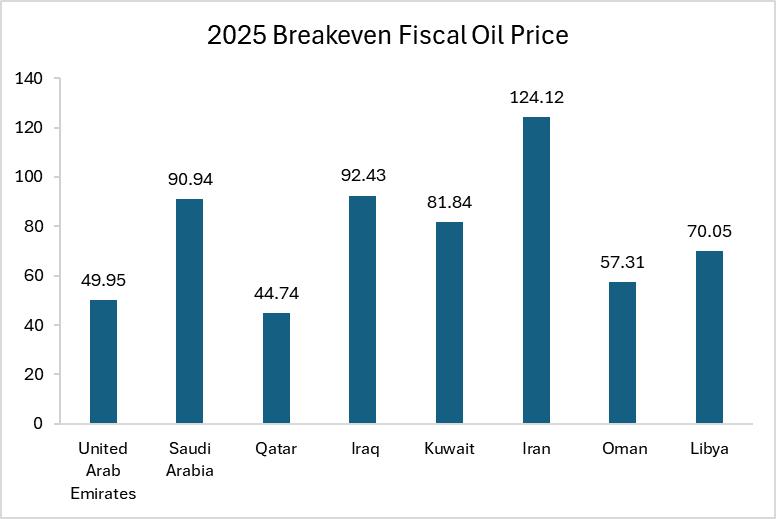

However, OPEC+ production policies remain the largest variable on the supply side. OPEC+ has extended its voluntary production cuts of 2.2 million barrels per day until the end of Q1 2025. Given that most OPEC countries require oil prices above $80 per barrel to balance their budgets, unless prices consistently remain above this level, the likelihood of continuing production cuts is high. Historical trends show OPEC+ tends to stabilize the market when Brent crude prices fall below $70 per barrel while increasing production becomes more likely when prices exceed $80 per barrel.

Source: IMF, Tradingkey.com

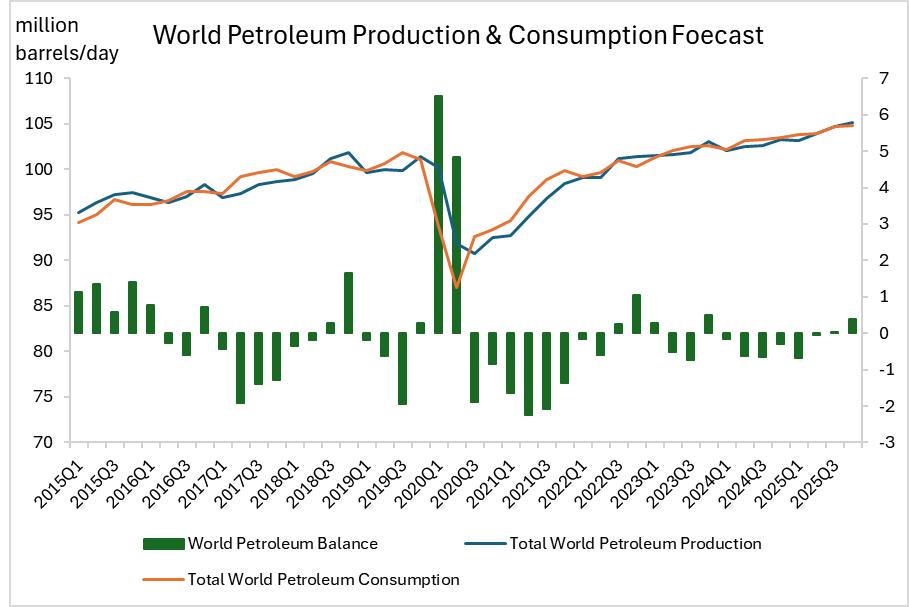

Based on supply-demand balance forecasts, global oil and other liquid fuels are expected to remain in a supply deficit in Q1 2025. However, from Q2, the supply-demand relationship is set to change significantly. With the release of new production capacity from non-OPEC countries, an oversupply is expected starting in Q2, with the surplus expanding further in Q3 and Q4.

Source: EIA, Tradingkey.com

This shift in supply-demand dynamics, coupled with OPEC+'s sensitivity to oil prices in adjusting production policies, means the oil market will face increased supply pressure in 2025. OPEC+ will need to strike a balance between maintaining market share and stabilizing prices.

Demand Side: China's New Phase and India's Rapid Expansion

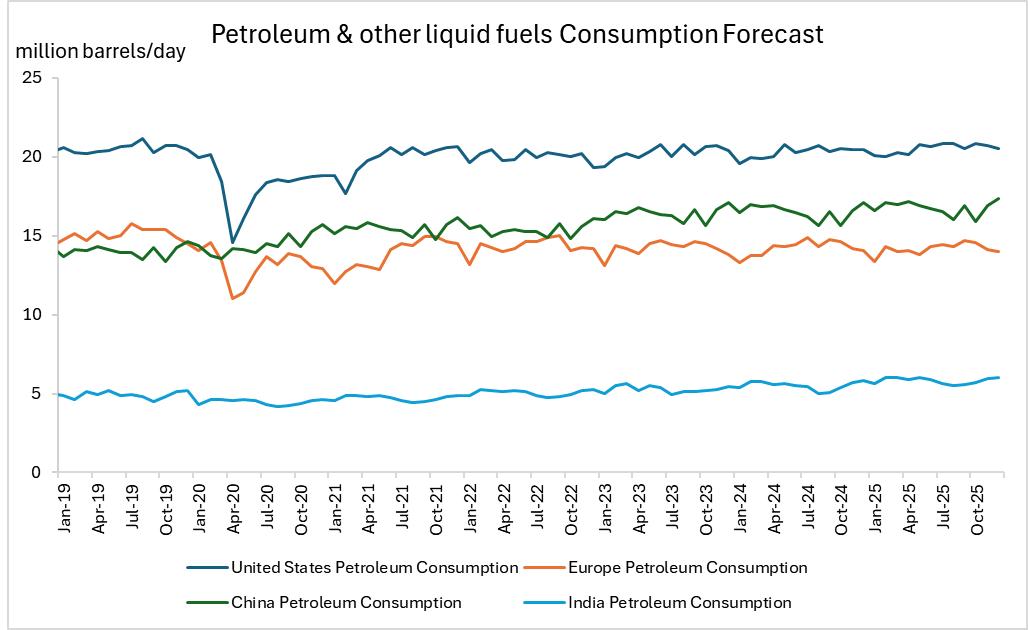

Global oil consumption patterns are undergoing significant changes. According to the latest EIA forecasts, global demand growth is expected to reach 1.3 million barrels per day in 2025. The performance of two major Asian economies stands out:

Source: EIA, Tradingkey.com

China's oil demand is entering a new phase. Despite government measures to boost the economy, demand growth in 2025 is projected to be only 280,000 barrels per day. This moderate growth reflects underlying structural changes - the rapid penetration of new energy vehicles (sales already exceeding 50% market share), population trends and moderate economic growth, which significantly limit traditional transportation fuel demand.

On the other hand, India's oil demand is set to surge. According to the latest EIA projections, India’s oil demand growth constitutes 25% of the global increase in oil demand, driven by the country's expanding middle class and increasing transportation needs.

However, China's consumption is still over three times larger, making it a pivotal factor in the global oil supply-demand balance. The contrast in growth trajectories between these two Asian giants will continue to shape the dynamics of the global oil market in 2025.

Inventory Status: Persistent Tightness

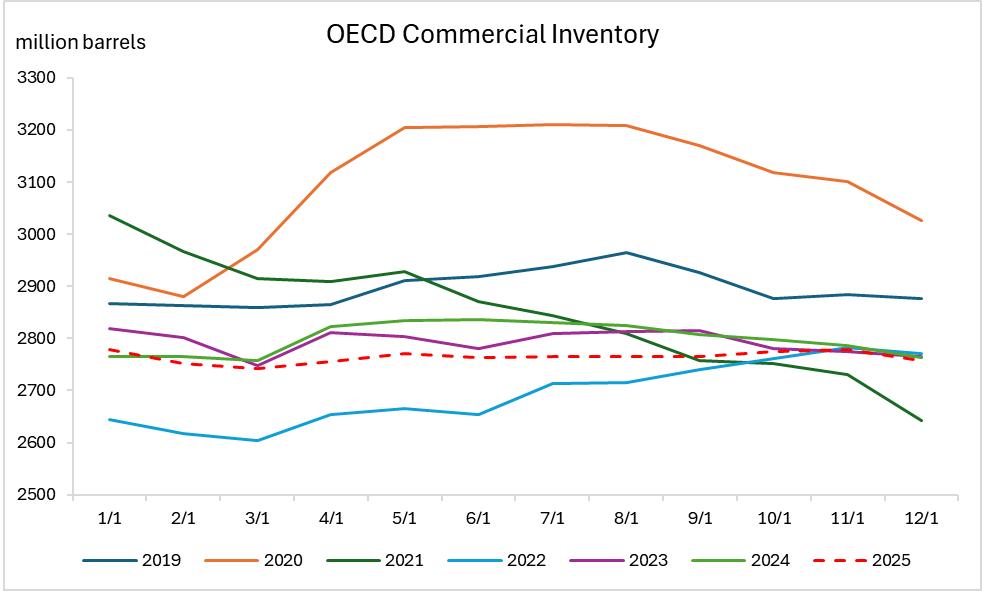

OECD commercial oil inventories in 2024 have remained near historical lows and this tight inventory situation is expected to persist into 2025. While this partly reflects a cooling of speculative market sentiment, low inventory levels also pose risks for price volatility. Particularly in the context of escalating geopolitical conflicts, low inventories could be leveraged by speculative capital to amplify upward price risks.

Source: EIA, Tradingkey.com

Crude Oil Conclusion

With supply gradually shifting towards oversupply but geopolitical risks remaining elevated, oil prices in 2025 are expected to follow a pattern of high in the first half, then lower. Geopolitical risk premiums and OPEC+ production cuts will drive prices in the first half and the second half, despite China's moderate demand recovery, global supply growth might outpace demand growth, putting downward pressure on prices.

Brent crude is projected to fluctuate within the $75-$85 per barrel range. An upward break would require further escalation in geopolitical risks or unexpectedly strong demand growth, while a downward break would need OPEC+ to abandon production cuts or a significant weakening in global demand.